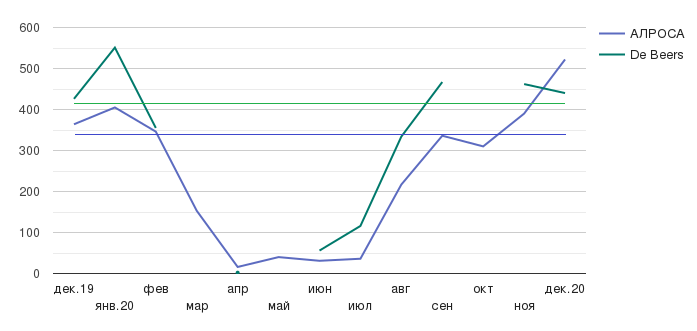

The year 2020 has become a serious issue for the global economy. The diamond mining industry was no exception. Lockdown and reduced diamond consumption, as well as uncertainty of the market outlook, slowed diamond sales to a low in the first quarter and bottomed out in the second quarter. Then the situation began to stabilize and in the fourth quarter, diamond sales volumes recovered to the level of the 4th quarter of 2019, exceeding the average sales volumes for the last 5 years in December.

Rough diamonds sales volumes of ALROSA and De Beers in 2020 compared to the average monthly sales in 2016-2019, million US dollars.

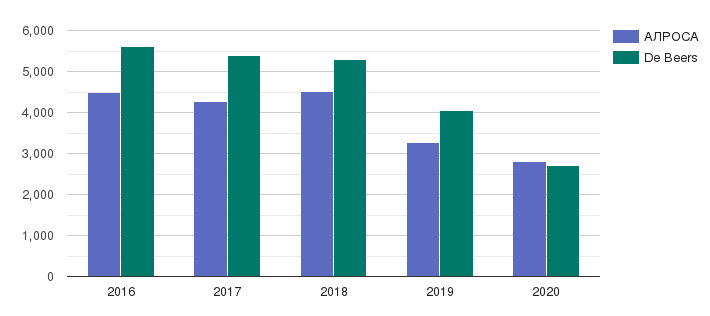

2/3 of the supply in the diamond market are regulated by 3 diamond mining companies: ALROSA, De Beers and Rio Tinto. The largest of them, ALROSA and De Beers, account for more than half of the world’s diamond production. ALROSA has significant reserves of diamonds, which it will develop for a long time. The share of De Beers is steadily declining due to the reduction of the mineral resource base. Rio Tinto’s share in the total production of natural diamonds in the world was 13-14%, but with the closure of the Australian Argyle field in the 4th quarter of 2020, the company’s production volumes in 2021 will decrease to 7 – 8 million carats, and in 2024 with the closure of the second Diavic portfolio field in Canada, the company may leave the market altogether along with 2 other large companies – Petra Diamond and Dominion Diamond Mines, which are experiencing serious difficulties due to a large credit load.

The volume of sales of diamonds by the largest diamond mining companies in 2016-2020, million US dollars.

The dominance of mining allows market makers to regulate the prices of rough diamonds, which means that the prices of diamonds are much less subject to volatility than the prices of other commodities, including gold and other precious metals and stones. Even a significant drop in demand due to the COVID-19 pandemic could significantly affect the prices of diamonds only in the low price group of up to $ 30 per carat, to some extent in the middle price group, and practically did not affect the prices of expensive rare stones, which is explained by the preservation of price lists by market makers based on the ‘price over volume’ policy – price priority over sales volumes.

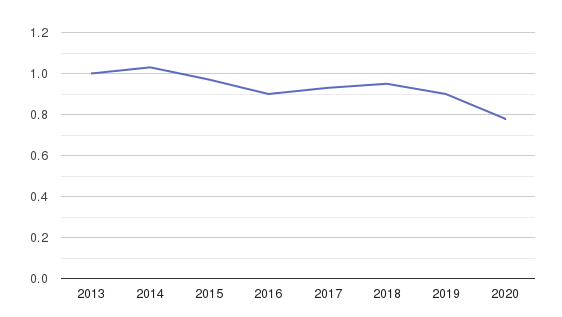

The average price index for ALROSA diamonds in comparable boxes, USD / carat.

The downside of this policy in the face of falling demand was the need to reduce the volume of sales of rough diamonds, which led to overstocking of warehouses from market makers. According to various estimates, the volume of diamonds in the warehouses of ALROSA has reached the annual production volume.

Large reserves of large diamond mining companies will gradually be realized, slowing the market recovery. However, this process occurs cyclically after each period of decline in demand and has long been traditional for the industry, so it will not bring unpleasant surprises. The sell-off of stocks to technological levels will continue until 2022, and given the continuation of the pandemic and the slow return of consumer demand, it may be delayed until 2023.

Small diamond mining companies cannot influence the market to such an extent as to bring down prices with a large volume of supply. Therefore, during periods of falling demand, when market makers are forced to limit sales to maintain the price level, ALMAR will be able to continue selling the extracted diamonds through long-term contracts with minimal losses in revenue.

The annual production volume of ALMAR will be 0.5 – 0.6% of the total diamond mining in the world. According to this indicator, the company will take a place in the second tier of diamond miners, represented mainly by companies from South Africa, and due to its Russian origin, it will stand out favorably in the eyes of buyers with greater stability and reliability, as well as a reputation as a supplier of “non-conflict” diamonds.

The range of ALMAR diamonds with an average value of more than $ 100 per carat at the Beenchime site and $ 25 – 30 per carat at the Khatystakhsky site, with an average global value of $ 130 per carat, corresponds to the demand of the Chinese and Indian markets, which provide 15% and 70% of the global demand for rough diamonds, respectively. Demand and prices for rough diamonds worth $ 100/carat are fairly stable, and demand for cheap raw materials in the range of up to $ 30 / carat will support the termination of Rio Tinto production at the world’s largest Argyle field in Australia in 2020, which is comparable in terms of the range and cost of raw materials to the Khatystakh field ALMAR.

The main factors that will influence the diamond mining industry in the future.

POSITIVE FACTORS

- Increase in the number of mature consumers (the main target audience of diamond jewelry).

- Consumption growth in the US, China and Japan.

- The cheaper technology for growing synthetic diamonds makes them more affordable and attracts new consumers (similar to cubic zirconia).

- Depletion of SMEs, decommissioning of large deposits, including the world’s largest Argyle field in 2020 (8% of global diamond production, 90% of pink diamond production, over 40 years of operation it produced 870 million carats of diamonds), the Diavik field in Canada in 2024, the withdrawal of the Mir pipe in Yakutia in 2017 (at least until 2030 due to an accident) , and others. At the same time, no new large deposits have been found that are comparable in reserves.

- Restoration of product branding at the level of De Beers ‘ expenses during the monopoly period ($200-220 million per year, 1% of the market volume).

- Recovery of the Indian diamond industry, reduction of the debt burden from 16% (2013) to 9-10%.

NEGATIVE FACTORS

- Changing the consumption paradigm in new generations.

- Reduced consumption in India, the Persian Gulf, and Europe.

- The development of technology for growing synthetic diamonds reduces the consumption of natural stones in the mass segment of inexpensive diamond jewelry and increases the cost of verification of natural diamonds.

- Gradual sale of stocks by upstream market makers.

- There are possible bankruptcies of several large upstream companies due to excessive debt load-Dominion Diamond Mines, Petra Diamonds.

Despite the fact that the coronavirus significantly affected the diamond mining industry in the field of sales reduction in 2020, and prices for ALMAR rough diamonds decreased slightly, these factors are temporary, which is confirmed by data on the market recovery since the fall of 2020, sales of ALROSA, De Beers and other diamond miners returned or exceeded the level of 2019.

We see a large window of opportunity for our company in the medium and long term, starting in 2024, in the 4th quarter of which sales of rough diamonds extracted from the ALMAR fields will begin. In particular, the company will be able to provide even greater stability and profitability by increasing its balance sheet reserves, optimizing expenses and increasing ruble revenue.